Con Law for 1Ls: NFIB v. Sebelius Explained

- Ashley M. Cornwell, Esq.

- Apr 24

- 8 min read

If Lopez, Morrison, and Raich are your modern Commerce Clause trilogy, NFIB v. Sebelius is the next major case because it asks:

Can Congress require people to buy health insurance?

The Supreme Court’s answer was complicated:

No, not under the Commerce Clause.

Yes, as an exercise of the Taxing Power.

And no, at least not in the way Congress tried to pressure states to expand Medicaid.

That is why National Federation of Independent Business v. Sebelius, 567 U.S. 519 (2012) is one of the biggest 1L cases in modern Constitutional Law.

This post is part of a Con Law for 1Ls series, so the goal is to make the case clear enough for class, cold calls, outlines, and exams.

The One-Sentence Takeaway

NFIB v. Sebelius held that the Affordable Care Act’s individual mandate could not be sustained under the Commerce Clause but could be upheld as a tax, while the Medicaid expansion was unconstitutionally coercive as written under the Spending Clause.

That is the short version to remember.

Why Your Professor Cares About NFIB

Your professor is not assigning NFIB just because it is politically famous. The real reason is that the case is a major constitutional crossroads.

It asks:

Can Congress regulate inactivity under the Commerce Clause?

When does a penalty count as a tax?

When does federal spending pressure become unconstitutional coercion of the states?

Few cases give you that much doctrine in one opinion.

That is why it is such a big Con Law case.

The Facts You Actually Need to Know

Here is the short 1L version.

The Affordable Care Act (ACA) included an individual mandate, requiring most Americans to maintain health insurance or pay a monetary exaction.

The law also dramatically expanded Medicaid, telling states that if they refused the expansion, they risked losing not just new Medicaid funds but also their existing Medicaid funding.

The ACA was challenged by states, individuals, and business groups.

The Supreme Court produced a complicated decision, but the key doctrinal results are very teachable.

The Three Big Issues

1. Commerce Clause

Could Congress require individuals to buy health insurance under its power to regulate interstate commerce?

2. Taxing Power

Could the payment required from those who declined insurance be treated as a tax?

3. Spending Clause / Medicaid

Could Congress condition continued Medicaid funding on states’ acceptance of the Medicaid expansion?

The Court split these issues up and answered them differently.

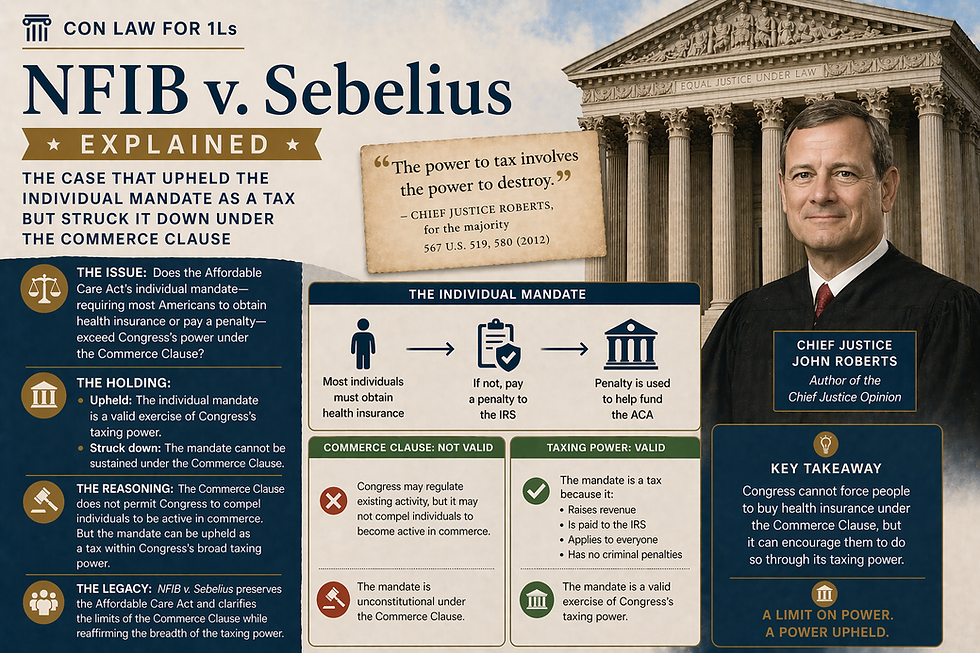

Issue One: The Commerce Clause

The question

Can Congress force people into commerce so that it can regulate them?

The Court’s answer

No.

Chief Justice Roberts concluded that the Commerce Clause lets Congress regulate existing commercial activity, but it does not allow Congress to compel individuals to become active in commerce by purchasing a product. See NFIB v. Sebelius.

That is one of the most important doctrinal points in the case.

Why the Commerce Clause Argument Failed

The government argued that everyone eventually participates in the healthcare market, and that uninsured people shift costs to others. Therefore, Congress could regulate the decision not to buy insurance.

The Court rejected that argument.

Why?

Because the Commerce Clause has always been understood to regulate activity, not force people into activity.

The Court worried that if Congress could regulate inactivity just because inactivity affects markets, then there would be no real limit on federal power.

That is the same federalism concern you saw in Lopez and Morrison, but now in a new form.

The Key Commerce Clause Rule in 1L Terms

Here is the exam-friendly version:

The Commerce Clause allows Congress to regulate economic activity, but it does not authorize Congress to compel individuals to enter commerce by purchasing a product.

That is the core Commerce Clause holding of NFIB.

Issue Two: The Taxing Power

This is the part that surprises a lot of students the first time they read the case.

The question

If the individual mandate cannot be upheld under the Commerce Clause, can it still survive as a tax?

The Court’s answer

Yes.

Chief Justice Roberts concluded that the payment required from people who went without health insurance functioned like a tax for constitutional purposes, even though Congress called it a “penalty” in the statute. See NFIB.

That is the move that saved the individual mandate.

Why the “Penalty” Could Still Count as a Tax

The Court looked at how the payment operated in practice.

It emphasized that the exaction:

was paid to the IRS,

was collected through normal tax mechanisms,

was not so punitive as to be a true criminal sanction,

and gave people a lawful choice: buy insurance or make the payment.

Because of how it functioned, the Court treated it as a tax for constitutional analysis.

That is an important point for exams:

Constitutional analysis can turn more on function than label.

The Key Taxing Power Rule in 1L Terms

Here is the clean rule:

A statutory exaction may be upheld as a tax if it functions like a tax, even if Congress labels it a penalty.

That is one of the most important doctrinal takeaways from the case.

Issue Three: Medicaid Expansion and the Spending Clause

This is the part many students forget, but it is hugely important.

The question

Can Congress pressure states to expand Medicaid by threatening them with the loss of all existing Medicaid funds if they refuse?

The Court’s answer

Not in that form.

The Court held that this arrangement was unconstitutionally coercive. Congress can attach conditions to federal funds, but here the financial threat was so severe that it crossed the line from encouragement to coercion. See NFIB.

That was a very significant Spending Clause holding.

Why the Medicaid Expansion Was a Problem

States argued that Medicaid had become such a large part of their budgets that threatening the loss of all existing funds was essentially a gun to the head.

The Court agreed.

It held that Congress can offer states new funds for new programs, but it cannot transform participation into something functionally non-optional by threatening a massive loss of existing funding.

So the Medicaid expansion was not struck down entirely. Instead, the Court limited the remedy:

the federal government could offer new expansion funds,

but it could not penalize states by taking away their preexisting Medicaid funding if they declined.

That is a very important distinction.

The Key Spending Clause Rule in 1L Terms

Here is the exam-friendly version:

Congress may encourage states through spending conditions, but it may not coerce them by threatening the loss of massive existing funding in a way that leaves no real choice.

That is the big Spending Clause takeaway from NFIB.

The Cold-Call Version

If your professor asks, “What is NFIB v. Sebelius about?” you can say:

NFIB v. Sebelius held that the Affordable Care Act’s individual mandate could not be upheld under the Commerce Clause because Congress cannot compel people into commerce, but the mandate could be upheld as a tax. The Court also held that the Medicaid expansion, as structured, was unconstitutionally coercive under the Spending Clause.

That is a strong cold-call answer.

How NFIB Fits with Lopez, Morrison, and Raich

This is the big doctrinal arc.

Lopez and Morrison:

Congress cannot regulate every local non-economic matter under the Commerce Clause.

Raich:

Congress still has broad power when regulating a comprehensive national market scheme.

NFIB:

Even broad commerce power has a further limit — Congress may regulate economic activity, but it cannot force people into commerce in the first place.

That is the key Commerce Clause contribution of NFIB.

So if your professor asks how NFIB fits into the sequence, that is the answer.

Why NFIB Is So Important

NFIB matters because it is one of the rare cases where the Court:

rejects a major federal power argument under one clause,

upholds the same statute under another clause,

and simultaneously creates an important new limit in spending-power doctrine.

That is a lot of constitutional law in one case.

It is especially important because it touches both:

federalism, and

the practical mechanics of constitutional interpretation

The case also reminds you that different constitutional powers are distinct. A law may fail under one source of power and survive under another.

Common 1L Mistakes About NFIB

Mistake #1: Saying the ACA “won” or “lost”

Too simplistic. Different parts of the statute were treated differently under different constitutional provisions.

Mistake #2: Thinking the case is only about the Commerce Clause

It is also a major Taxing Power and Spending Clause case.

Mistake #3: Thinking the Court said Congress can never influence private decisions

Not quite. Congress may often influence behavior through taxes. The Court’s point was narrower: Congress cannot compel commerce under the Commerce Clause.

Mistake #4: Forgetting the Medicaid holding

The Medicaid coercion ruling is one of the biggest doctrinal parts of the case.

Quick IRAC for Your Outline

Issue

Could Congress constitutionally enact the ACA’s individual mandate and Medicaid expansion?

Rule

Congress may regulate economic activity under the Commerce Clause, but it may not compel inactivity into commerce. A payment may be upheld as a tax if it functions like one. Congress may attach conditions to federal spending, but may not coerce states through overwhelming financial threats. See NFIB.

Application

The individual mandate could not be justified under the Commerce Clause because it compelled individuals to enter the insurance market. But the payment for going uninsured functioned sufficiently like a tax to be upheld under the Taxing Power. The Medicaid expansion, however, was coercive because states risked losing huge existing Medicaid funds if they refused to participate.

Conclusion

The mandate survived as a tax, but the Medicaid expansion could not be enforced through that coercive funding threat.

What to Put in Your Case Brief

If you are briefing NFIB for class, include:

Facts: ACA individual mandate and Medicaid expansion challenged

Issue 1: Commerce Clause

Holding 1: no, Congress cannot compel people into commerce

Issue 2: Taxing Power

Holding 2: yes, the exaction functions like a tax

Issue 3: Spending Clause / Medicaid

Holding 3: the funding threat was unconstitutionally coercive

Key doctrine: activity/inactivity distinction, functional tax analysis, anti-coercion spending principle

That is enough for most 1L purposes.

Why NFIB Still Matters Today

NFIB remains hugely important because it is central to modern debates over:

the limits of federal regulatory power,

the difference between taxes and penalties,

and the constitutional line between encouragement and coercion in cooperative federalism programs.

It is also still discussed in later ACA litigation and in federalism cases more broadly. See, for example, California v. Texas, 141 S. Ct. 2104 (2021), which revisited ACA-related issues after the penalty was reduced to zero.

How NFIB Fits with the Earlier Cases

By this point, your federal power sequence looks like this:

McCulloch: federal power can be broad

Gibbons: the commerce power can be broad

Lopez: there are limits on the commerce power

Morrison: those limits apply to non-economic private violence

Raich: Congress can still reach local conduct as part of a broader economic regulatory scheme

NFIB: but Congress cannot compel people into commerce, and spending power also has coercion limits

That is a very strong 1L outline arc.

Final Takeaway for 1Ls

If you remember nothing else, remember this:

NFIB v. Sebelius says that Congress cannot use the Commerce Clause to force people into the marketplace, but it may sometimes influence behavior through its taxing power, and it cannot coerce states through spending conditions that leave them no real choice.

That is why the case matters so much.

The ACA was the vehicle.The real subjects were the limits of the Commerce Clause, the reach of the Taxing Power, and the boundary between encouragement and coercion under the Spending Clause.

And that is why NFIB v. Sebelius, 567 U.S. 519 (2012) is one of the core Con Law cases every 1L should know.

Comments